How Do I Make My Car Payment

Alright, let's talk about something as crucial as turning a wrench: making your car payment. It might not involve carburetors or coil-overs, but understanding the process, especially the digital systems involved, can save you headaches, prevent late fees (which are basically money down the drain), and even help you negotiate better terms in the future. This article will break down the modern car payment process, focusing on the electronic fund transfers and online systems that are now standard.

Purpose: Avoiding the Wrench in Your Financial Gears

Why bother understanding this? Well, beyond the obvious of avoiding repossession, knowing how your payment system works helps in a few key ways:

- Troubleshooting Payment Issues: If a payment is missed or delayed, you'll be better equipped to diagnose the problem – is it your bank, the lender's system, or a simple user error?

- Optimizing Payment Timing: Understanding when your payment actually posts allows you to manage your cash flow more effectively. Some systems allow you to adjust payment dates to better align with your payday.

- Security Awareness: Knowing the digital pathways of your money helps you identify and avoid potential scams and protect your financial information.

- Negotiating Power: In some cases, understanding the internal processes of the lender can give you leverage when discussing loan modifications or deferments.

Think of this as preventative maintenance for your financial health. Just like you wouldn't ignore a squealing belt, you shouldn't ignore understanding where your hard-earned money is going.

Key Specs and Main Parts of the Modern Car Payment System

The car payment process, in its simplest form, involves a transfer of funds from your bank account to the lender. However, the backend is more complex, involving various systems and players.

Key Specs:

- ACH (Automated Clearing House): The backbone of most electronic car payments in the US. ACH is a network that facilitates electronic funds transfers between banks.

- NACHA (National Automated Clearing House Association): The organization that governs the ACH network. They set the rules and standards for electronic payments.

- API (Application Programming Interface): Many lenders use APIs to connect their systems to payment gateways and banks, automating the payment process.

- SSL/TLS Encryption: Critical for securing your financial information when transmitted online. Look for the padlock icon in your browser's address bar.

Main Parts:

- Your Bank Account: The source of funds. Requires a valid account number and routing number.

- Payment Gateway: A service that securely processes online payments. Examples include PayPal, Stripe, and proprietary gateways used by lenders.

- Lender's System: The software used by the lender to manage loan accounts, track payments, and generate reports.

- ACH Network: The infrastructure that moves funds between your bank and the lender's bank.

Symbols and Flow

While there isn't a single, standardized "car payment diagram," we can visualize the flow of funds and data. Imagine a simplified flow chart:

[You (Your Bank Account)] --> [Payment Initiation (Online Portal/Autopay)] --> [Payment Gateway (Encryption)] --> [ACH Network] --> [Lender's Bank Account] --> [Lender's System (Loan Account Updated)]

Key symbols used in similar flowcharts might include:

- Solid Arrows: Represent the flow of funds or data.

- Dashed Lines: Could indicate a potential security risk or area for error.

- Cloud Icon: Often represents a cloud-based service, such as a payment gateway or lender's online portal.

- Lock Icon: Indicates encryption and secure data transmission.

How It Works: The Electronic Money Trail

Let's break down the process step-by-step:

- You Initiate Payment: You log into the lender's online portal, set up autopay, or initiate a one-time payment. This involves providing your bank account information (account number and routing number).

- Payment Gateway Takes Over: The payment gateway securely collects your financial information and encrypts it using SSL/TLS encryption. This protects your data from being intercepted during transmission.

- ACH Request is Generated: The payment gateway creates an ACH debit request, which authorizes the transfer of funds from your bank account.

- ACH Network Processes the Request: The ACH network routes the debit request to your bank.

- Your Bank Approves/Denies: Your bank verifies that you have sufficient funds and approves the debit request. If there are insufficient funds (NSF), the payment will be rejected, and you may incur fees from both your bank and the lender.

- Funds are Transferred: Once approved, the funds are transferred from your bank account to the lender's bank account through the ACH network.

- Lender Updates Your Account: The lender's system receives notification that the payment has been received and updates your loan account balance.

The entire process typically takes 1-3 business days. This "float time" is important to keep in mind when scheduling payments.

Real-World Use: Troubleshooting Common Payment Problems

Let's say you get a late payment notice. What do you do?

- Check Your Bank Account: Was the payment actually debited? Look for the transaction on your bank statement.

- Review Payment History on Lender's Portal: Did the lender receive the payment? Their system should show a record of all transactions.

- Verify Bank Account Information: Double-check that the account number and routing number are correct. A typo can cause the payment to fail.

- Contact Your Bank: If the payment was debited from your account but not received by the lender, contact your bank to investigate. They can trace the transaction and identify any errors.

- Contact the Lender: If the payment was rejected due to NSF, deposit sufficient funds into your account and try again. You may need to pay a late fee.

Important Note: Always document your communications with both your bank and the lender. Keep records of dates, times, and names of representatives you speak with. This documentation can be invaluable if you need to dispute a charge or resolve a payment issue.

Safety: Guarding Your Financial Data

The biggest risk associated with online car payments is phishing scams. Be wary of emails or phone calls claiming to be from your lender requesting your bank account information. Never provide your financial information unless you are absolutely sure you are on the lender's legitimate website or speaking to a verified representative.

Here are some key safety tips:

- Use Strong Passwords: Create complex passwords for your online accounts and don't reuse passwords across multiple sites.

- Enable Two-Factor Authentication (2FA): If your lender offers 2FA, enable it. This adds an extra layer of security to your account.

- Monitor Your Bank Account: Regularly check your bank statements for any unauthorized transactions.

- Beware of Suspicious Emails: Don't click on links or open attachments in emails from unknown senders.

- Keep Your Software Up-to-Date: Ensure your web browser and operating system are up-to-date with the latest security patches.

Remember, your financial information is valuable. Take steps to protect it.

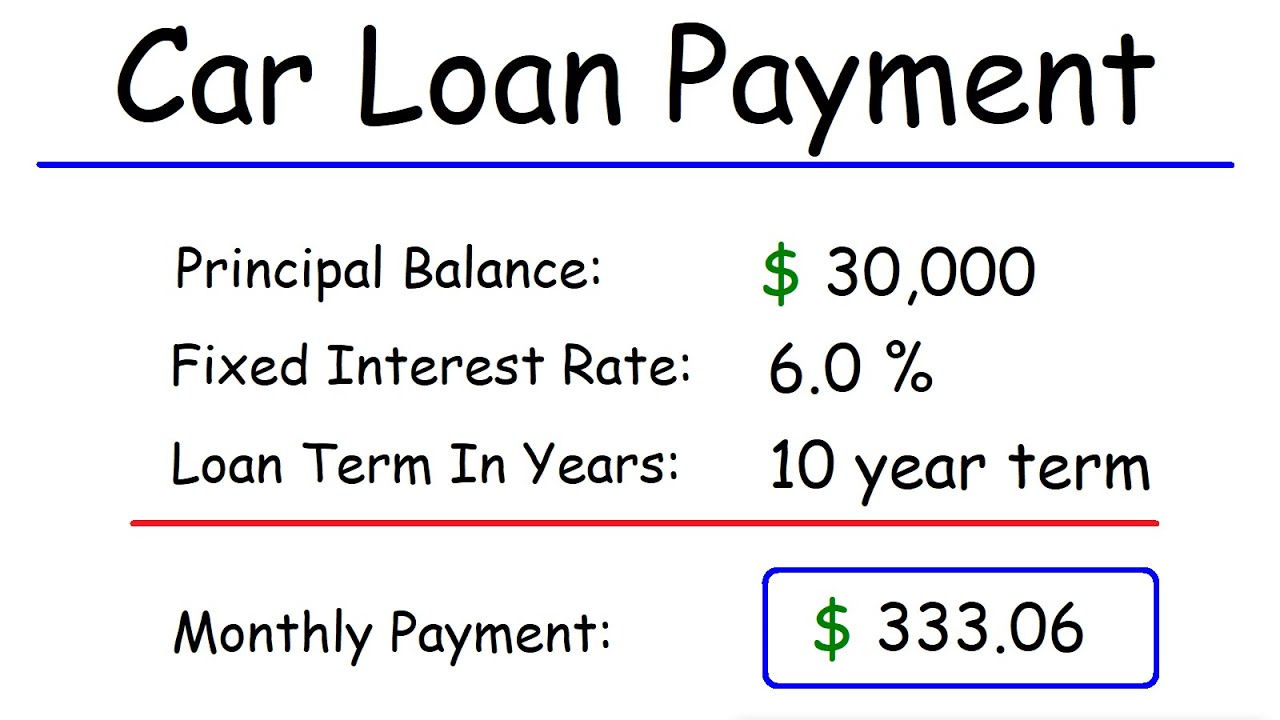

We have a simplified diagram of the car payment process, including key checkpoints and data flow. You can download it here to further enhance your understanding.