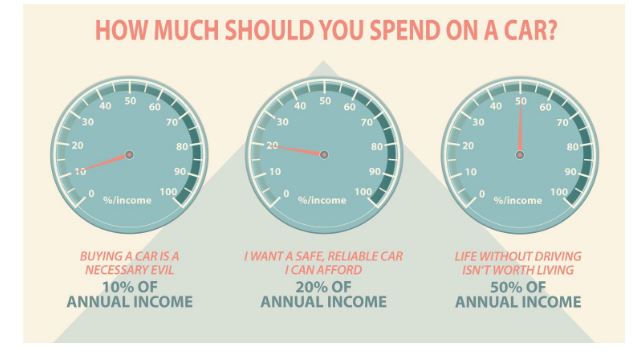

How Much Car Payment Will Be

Alright, let's talk car payments. Figuring out how much you'll actually be shelling out each month isn't as simple as just looking at the sticker price of the vehicle. There are a bunch of factors at play, and understanding them is crucial whether you're budgeting for a new ride, refinancing an existing loan, or just trying to get a handle on your finances.

Purpose – Why Understanding Car Payments Matters

Why bother diving into the nitty-gritty of car payment calculations? Well, for starters, it helps you avoid getting ripped off. Dealers and lenders sometimes use deceptive tactics, and being informed is your best defense. Knowing how the payment is derived also empowers you to:

- Accurately Budget: Predictable expenses are key to financial stability.

- Negotiate Effectively: Understanding the terms allows you to negotiate better interest rates or loan durations.

- Make Informed Decisions: Determine if you can realistically afford the vehicle.

- Refinance Strategically: Knowing your current loan terms is essential when considering refinancing options.

Key Specs and Main Parts of a Car Payment Calculation

The core of a car payment calculation relies on a few key figures. These figures are then plugged into a formula that tells you what your monthly obligation will be. Here's a breakdown:

- Principal (P): This is the loan amount, or the total amount you're borrowing. It's the vehicle's price minus any down payment, trade-in value, or rebates. Get this wrong, and the whole calculation is off.

- Interest Rate (r): Expressed as an annual percentage rate (APR), this is the cost of borrowing money. It's crucial to shop around for the best rate, as it significantly impacts your total cost over the loan's lifetime. Remember, APR includes not just the interest rate, but other loan fees too.

- Loan Term (n): The length of the loan, usually expressed in months (e.g., 60 months for a 5-year loan). Longer terms mean lower monthly payments, but you'll pay significantly more in interest over the life of the loan. Shorter terms mean higher payments, but lower overall cost.

The Car Loan Formula: This is the workhorse of the calculation. The formula itself might look intimidating, but breaking it down makes it manageable.

M = P [ r(1 + r)^n ] / [ (1 + r)^n – 1]

Where:

- M = Monthly Payment

- P = Principal Loan Amount

- r = Monthly Interest Rate (Annual Rate / 12)

- n = Number of Months in the Loan Term

Don't panic! You don't have to do this by hand. There are plenty of online car loan calculators that do the heavy lifting. But understanding the formula lets you double-check the calculator's output and understand how changes in each variable affect your payment.

Other Factors Affecting Your Total Cost

While the formula gives you the core payment, other things get tacked on to the overall amount:

- Sales Tax: This varies by state and sometimes locality, and it's a percentage of the vehicle's price.

- Fees: Dealerships love to add fees: documentation fees, processing fees, etc. Many of these are negotiable, so don't be afraid to push back.

- Insurance: Required by law (and common sense), car insurance is a significant monthly expense.

- Gap Insurance: Recommended if you're financing a large percentage of the vehicle's value. It covers the difference between what you owe on the loan and what the car is worth if it's totaled.

How It Works: A Step-by-Step Example

Let's say you're buying a car for $25,000. You put down $5,000, leaving a principal loan amount (P) of $20,000. You secure an interest rate (r) of 6% APR, and you opt for a 60-month loan term (n).

- Calculate the Monthly Interest Rate: 6% APR / 12 months = 0.005 (or 0.5% monthly).

- Plug the Values into the Formula: M = 20000 [ 0.005(1 + 0.005)^60 ] / [ (1 + 0.005)^60 – 1]

- Solve for M: (Using a calculator, of course!) M ≈ $386.66

So, your estimated monthly payment before taxes and fees would be approximately $386.66. Remember to add in those other expenses to get a true picture of your total monthly cost.

Real-World Use – Basic Troubleshooting Tips

Okay, so you've calculated your payment, but what if things don't quite match up? Here are some troubleshooting tips:

- Double-Check the Inputs: The most common error is incorrect data. Make sure you're using the correct principal, interest rate, and loan term.

- Compare Quotes: Get multiple loan quotes from different lenders (banks, credit unions, online lenders) to ensure you're getting the best possible rate.

- Read the Fine Print: Dealers often include add-ons (extended warranties, service contracts) that inflate the loan amount and, therefore, your payment. Carefully review the loan documents before signing.

- Negotiate Everything: Don't be afraid to negotiate the price of the vehicle, the interest rate, and those pesky fees. Dealers expect you to negotiate.

- Consider Refinancing: If interest rates drop after you take out your loan, refinancing can lower your monthly payment and save you money over the long term.

- Beware of Scams: If a deal sounds too good to be true, it probably is. Watch out for lenders that require large upfront fees or pressure you into signing quickly.

Safety – Highlight Risky Components (of the loan, not the car!)

The riskiest components of a car loan aren't mechanical; they're financial. Pay close attention to these warning signs:

- High Interest Rates: A high APR (anything above the current average for your credit score) means you'll pay significantly more in interest over the life of the loan.

- Long Loan Terms: While lower monthly payments are tempting, longer loan terms mean you'll be paying interest for a longer period, and you could end up owing more than the car is worth.

- Upside-Down Loans: This happens when you owe more on the car than it's worth, making it difficult to sell or trade in. Avoid this by making a substantial down payment and choosing a shorter loan term.

- Hidden Fees: Be wary of dealers who try to sneak in extra fees without clearly explaining them. Demand a breakdown of all costs before signing anything.

- Poor Credit Impact: Missing car payments can severely damage your credit score, making it difficult to obtain loans or credit in the future.

By being proactive, knowing your numbers, and understanding how a car loan works, you can make a smart and informed decision. Take your time, do your research, and don't be afraid to walk away from a bad deal.

Remember, a successful car purchase isn't just about getting the right vehicle; it's about getting the right financial package. We've got a car payment calculation diagram available for download. It visually lays out the formula and key variables, making it even easier to understand. Use it as a reference when negotiating your next car deal.