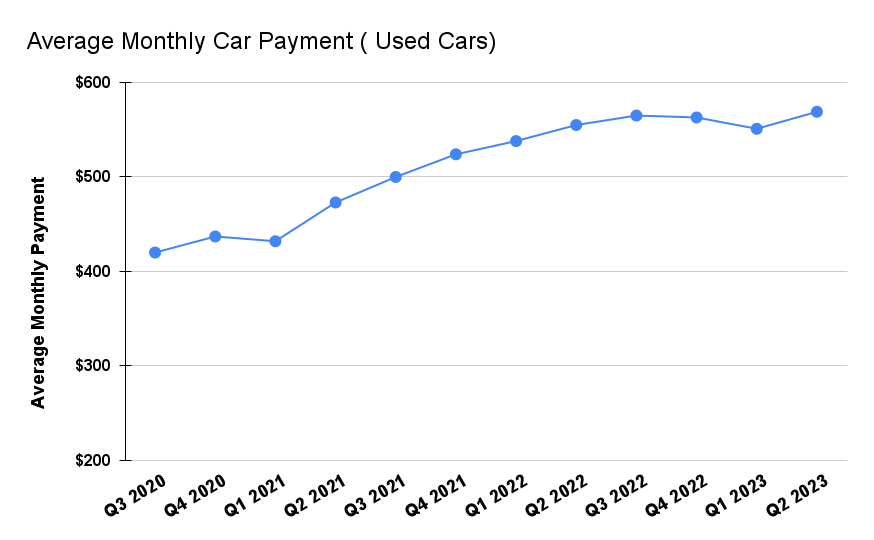

How Much Is Average Car Payment

Understanding the average car payment is more than just knowing a number; it's about grasping the underlying economic factors that influence your monthly automotive expenses. This knowledge empowers you to make informed decisions when buying a new or used vehicle, renegotiating financing, or even assessing the overall affordability of car ownership. Think of it as diagnosing a complex engine problem – you need to know the components to understand the bigger picture.

Why Understanding Average Car Payments Matters

Knowing the average car payment offers several key advantages:

- Budgeting and Financial Planning: You can realistically estimate your potential car expenses and adjust your budget accordingly.

- Negotiating Power: Understanding the average helps you assess the fairness of the financing options presented by dealers and lenders.

- Refinancing Opportunities: If you’re paying significantly more than the average, refinancing your loan could save you money.

- Vehicle Selection: It helps you determine which types of vehicles are within your budget. Maybe that dream sports car is out of reach, but a reliable sedan might be a smarter choice.

- Long-Term Financial Health: Overspending on a car can negatively impact your overall financial health. Knowledge of average payments helps prevent this.

Key Specs and Influencing Factors

The "average" car payment isn't a static figure; it fluctuates based on a variety of factors. Think of these as the variables in a complex equation. Here are some of the most important:

- New vs. Used Cars: New cars typically command higher prices, leading to larger loan amounts and therefore higher monthly payments. Used cars offer lower purchase prices, but interest rates might be higher, and shorter loan terms can impact the monthly payment.

- Loan Term: The loan term (the length of time you have to repay the loan) significantly affects the monthly payment. Longer terms result in lower monthly payments but higher overall interest paid. Shorter terms mean higher monthly payments but lower total interest. This is a classic trade-off.

- Interest Rate (APR): The Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a percentage. A higher APR translates directly to a higher monthly payment and significantly more interest paid over the life of the loan. Your credit score heavily influences your APR.

- Down Payment: The amount of money you put down upfront reduces the loan amount, resulting in a lower monthly payment. A larger down payment also demonstrates financial responsibility to lenders, potentially leading to a better APR.

- Credit Score: Your credit score is a numerical representation of your creditworthiness. A higher credit score generally qualifies you for lower interest rates. A lower score, conversely, can lead to higher rates or even loan denial.

- Vehicle Type and Trim Level: The type of vehicle (sedan, SUV, truck) and its trim level (base model, luxury edition) significantly impact the purchase price. Luxury vehicles with advanced features command higher prices.

- Location: Sales taxes and registration fees can vary significantly by state and even local jurisdictions.

- Incentives and Rebates: Manufacturer incentives and rebates can reduce the purchase price, lowering the loan amount.

Understanding Common Terminology

To fully understand the factors influencing car payments, you need to be familiar with some key financial terms:

- Principal: The original amount of the loan before interest is applied.

- Interest: The cost of borrowing money.

- APR (Annual Percentage Rate): The annual rate charged for borrowing money, including fees and other costs.

- Loan Term: The length of time you have to repay the loan.

- Depreciation: The decrease in value of a vehicle over time.

- Equity: The difference between the value of the vehicle and the outstanding loan balance.

- LTV (Loan-to-Value) Ratio: The ratio of the loan amount to the value of the vehicle.

How Average Car Payments Are Calculated

The average car payment is typically calculated using a simple loan amortization formula. While online calculators are readily available, understanding the formula provides deeper insight:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Monthly Payment

- P = Principal Loan Amount

- i = Monthly Interest Rate (Annual Interest Rate / 12)

- n = Number of Months (Loan Term in Years * 12)

This formula factors in the loan amount, interest rate, and loan term to determine the monthly payment. Keep in mind that this is a simplified calculation and doesn't account for taxes, fees, or insurance costs.

Real-World Use: Troubleshooting High Car Payments

If you're currently struggling with high car payments, here are some troubleshooting steps:

- Review Your Loan Documents: Carefully examine your loan agreement to understand the APR, loan term, and any associated fees. Understanding the fine print is crucial.

- Check Your Credit Score: Obtain a copy of your credit report to identify any errors or areas for improvement. Addressing negative items can significantly improve your credit score over time.

- Refinance Your Loan: Shop around for better interest rates from different lenders. Even a small reduction in APR can save you a substantial amount of money over the life of the loan.

- Consider Trading Down: If your current vehicle is too expensive, consider trading it in for a less expensive model.

- Accelerate Payments: If possible, make extra payments towards the principal to reduce the loan balance faster and shorten the loan term.

Safety Considerations

While dealing with car payments doesn’t involve physical risk in the same way as, say, working under a car, there are still financial safety aspects to consider:

- Predatory Lending: Be wary of lenders offering unusually high interest rates or unfavorable loan terms, especially if you have a low credit score. These lenders may be engaging in predatory lending practices.

- Overextending Yourself: Don't purchase a vehicle that you can't realistically afford. Overextending yourself financially can lead to financial stress and potential repossession.

- Hidden Fees: Carefully review all loan documents for hidden fees or charges.

It's always a good idea to consult with a financial advisor before making any major financial decisions, such as purchasing a car. They can help you assess your financial situation and develop a plan that meets your individual needs and goals.

We hope this detailed explanation has provided you with a solid understanding of the factors influencing average car payments and how to manage your automotive expenses effectively. Remember, knowledge is power when it comes to making smart financial decisions.

We have a detailed PDF file summarizing this information and providing links to useful resources. You can request it by contacting us through our website.