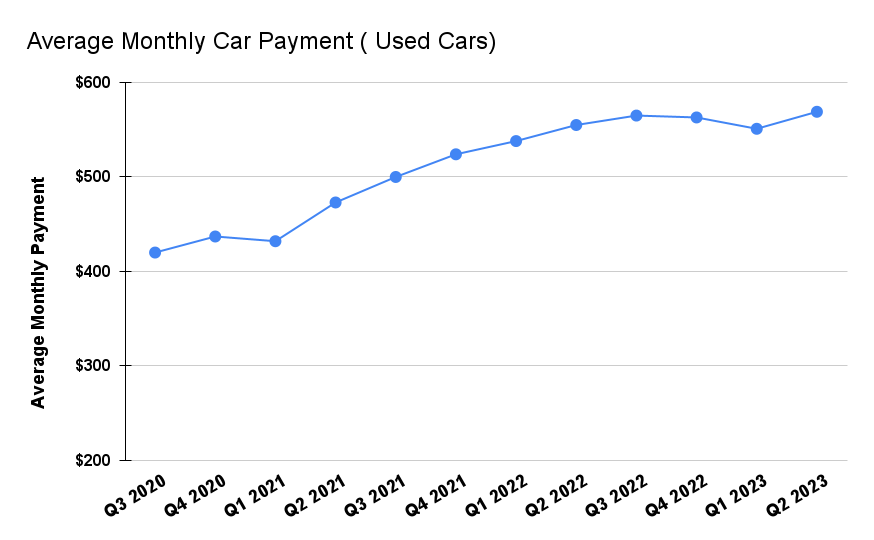

How Much Is The Average Car Note

Let's dive into a topic that's likely on the minds of many car owners: the average car note. Understanding the factors that contribute to this figure and how it affects your budget is crucial, whether you're a seasoned DIY mechanic or just starting to tinker with your ride. We'll break down the key components that make up the average car payment, explore influencing factors, and provide insights that can help you make informed decisions.

What Determines the Average Car Note?

The "average car note" isn't a fixed number; it's a statistical representation that fluctuates based on a multitude of economic and personal factors. Understanding these factors is key to interpreting the average and applying it to your individual situation. The purpose of understanding these factors are primarily to make better and financially savvy purchasing decisions for vehicles.

Key Specs and Main Parts

Several primary factors play a significant role in determining the average car note. These can be broken down into key components:

- Purchase Price: The sticker price of the vehicle, before any taxes, fees, or trade-ins, is the foundation of the loan. A higher purchase price directly translates to a larger loan amount and, consequently, a higher monthly payment.

- Interest Rate (APR): The Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a yearly percentage. It includes not only the interest rate but also other fees associated with the loan. A higher APR will increase your monthly payment and the total amount you pay over the life of the loan. Your credit score heavily influences the APR you'll receive.

- Loan Term: This is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term results in lower monthly payments but higher total interest paid over the loan's life. Conversely, a shorter loan term means higher monthly payments but less interest paid overall.

- Down Payment: The amount of money you pay upfront reduces the loan amount and can potentially lower your monthly payment. A larger down payment demonstrates to lenders that you're a lower risk borrower, which may result in a more favorable APR.

- Credit Score: Your credit score is a numerical representation of your creditworthiness, based on your credit history. A higher credit score indicates a lower risk of default, making you eligible for lower interest rates.

- Type of Vehicle: New cars typically have lower interest rates than used cars, but their higher purchase prices often lead to larger loan amounts. Luxury vehicles and those with advanced technology often command higher prices, increasing monthly payments.

- Regional Differences: The average car note can vary significantly depending on where you live. Factors like state taxes, dealer incentives, and cost of living can all play a role.

Symbols – Demystifying the Data

When reviewing average car note data, you'll encounter various symbols and metrics. Understanding these is essential for interpreting the information accurately:

- $: Represents monetary values, such as the average monthly payment or the total loan amount.

- %: Indicates percentages, such as the APR or the percentage of borrowers with a specific credit score.

- Months: Represents the loan term.

- Median vs. Average: The average is calculated by summing all values and dividing by the number of values. The median is the middle value when the values are arranged in order. The median is often a better representation of the "typical" car note because it's less sensitive to outliers (extremely high or low values).

How the Numbers Work Together

These components are interconnected and collectively determine the average car note. For instance, a low APR can offset the impact of a higher purchase price to some extent. Similarly, a larger down payment can significantly reduce the loan amount and monthly payment, regardless of the APR.

Lenders use complex algorithms to assess risk and determine loan terms and APRs. These algorithms consider your credit score, income, debt-to-income ratio (DTI), and other factors to evaluate your ability to repay the loan. A lower DTI and a higher credit score generally translate to more favorable loan terms.

Real-World Use – Basic Troubleshooting Tips

While you can't directly control the average car note, you can take steps to manage your own car loan:

- Improve Your Credit Score: Before applying for a car loan, check your credit report and address any errors. Pay your bills on time, keep your credit utilization low, and avoid opening too many new credit accounts in a short period.

- Shop Around for Loans: Don't settle for the first loan offer you receive. Compare offers from different lenders, including banks, credit unions, and online lenders. Look for the lowest APR and the most favorable loan terms.

- Negotiate the Purchase Price: Research the market value of the vehicle you're interested in and be prepared to negotiate the price with the dealer. Consider using online resources to find the best deals.

- Make a Larger Down Payment: Saving up for a larger down payment can significantly reduce your loan amount and monthly payment.

- Consider a Shorter Loan Term: While the monthly payments will be higher, you'll save money on interest in the long run and own your car outright sooner.

- Refinance Your Loan: If your credit score has improved since you took out your original car loan, consider refinancing to a lower APR. This can save you money on interest and lower your monthly payment.

Safety – Risky Financing Components

Certain financing practices can be risky and should be approached with caution:

- Extended Loan Terms (72+ months): While they offer lower monthly payments, extended loan terms can result in you owing more than the car is worth (being "upside down" on the loan) for a significant portion of the loan's life. This can be problematic if you need to sell or trade in the vehicle.

- High Interest Rates: Extremely high APRs can make it difficult to repay the loan and can lead to financial hardship. Be wary of lenders that offer loans with unusually high interest rates, especially if you have a less-than-perfect credit score.

- Balloon Payments: A balloon payment is a large lump-sum payment due at the end of the loan term. These payments can be difficult to manage and can leave you scrambling to find the funds to pay them off.

- Adding Extras to the Loan: Dealers may try to add extras like extended warranties or service contracts to your loan. While these may seem appealing, they can significantly increase your monthly payment and may not be worth the cost. Evaluate each item carefully before agreeing to add it to the loan.

Conclusion

Understanding the average car note and the factors that influence it empowers you to make informed decisions when financing a vehicle. By improving your credit score, shopping around for loans, negotiating the purchase price, and making a larger down payment, you can potentially lower your monthly payment and save money on interest. Remember to approach risky financing practices with caution and to carefully evaluate all loan terms and conditions before signing on the dotted line.

We have compiled a detailed diagram illustrating the interconnectedness of these factors influencing your car note. It also includes an interactive calculator to estimate monthly payments and total interest paid. This can be a valuable resource for further exploration and planning your next car purchase.