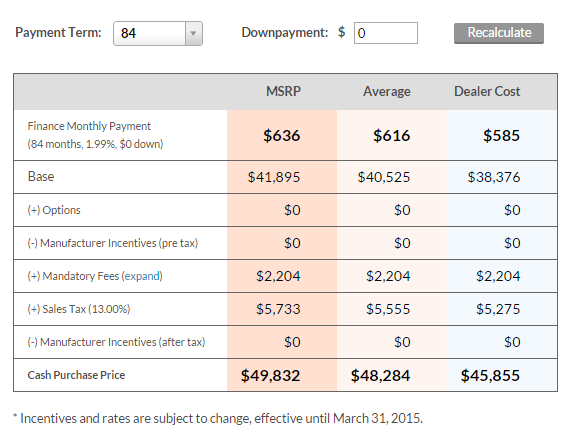

How Much Is The Monthly Payment

Alright, let's dive into figuring out that monthly car payment. This isn’t just about knowing the number; it's about understanding the underlying mechanics so you can negotiate better deals, plan your finances effectively, and even refinance with confidence down the road. Think of this as disassembling the engine of your loan – knowing each part helps you diagnose problems and keep things running smoothly.

Purpose: Decoding Your Loan & Future Proofing

Why bother understanding your monthly car payment calculation? Several reasons. First, it gives you the power to verify the accuracy of the loan agreement presented by the dealer or lender. Second, knowing the components allows you to explore refinancing options with greater clarity. Finally, it's essential for long-term financial planning, as your car loan significantly impacts your budget.

For those of you who enjoy modifying your rides, knowing your payment structure allows you to factor in potential modifications costs against your monthly expenses. Planning ahead helps prevent financial strain later on.

Key Specs and Main Parts: The Loan Formula

The core of any car payment calculation lies in the following formula. It may look intimidating at first, but we'll break it down:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Your monthly payment

- P = The principal loan amount (the amount you borrow)

- i = The monthly interest rate (annual interest rate divided by 12)

- n = The number of months in the loan term

Let's define these components in more detail:

- Principal Loan Amount (P): This is the initial amount you're borrowing. It's the price of the car minus any down payment, trade-in value, or rebates. A larger down payment reduces the principal and, consequently, the monthly payment.

- Annual Percentage Rate (APR): This is the annual interest rate charged on your loan. APR is crucial as it includes not only the interest rate but also any fees associated with the loan, giving you a true cost of borrowing. Be wary of low interest rates with hidden fees.

- Monthly Interest Rate (i): You can calculate this by dividing the APR by 12 (the number of months in a year). For example, if your APR is 6%, your monthly interest rate (i) is 0.06 / 12 = 0.005.

- Loan Term (n): This is the length of the loan, expressed in months. Common loan terms are 36, 48, 60, and 72 months. A longer loan term results in lower monthly payments but higher overall interest paid. Conversely, a shorter loan term means higher monthly payments but less total interest.

Dissecting the Formula: How It Works

The formula works by calculating the present value of a series of equal payments (your monthly payments) needed to repay the principal loan amount with interest over the loan term. Let’s break it down step-by-step:

- (1 + i)^n: This calculates the compound interest factor over the loan term. It represents how much the initial dollar grows over the loan term, considering the monthly interest rate.

- i(1 + i)^n: This multiplies the compound interest factor by the monthly interest rate.

- (1 + i)^n - 1: This subtracts 1 from the compound interest factor.

- [ i(1 + i)^n ] / [ (1 + i)^n – 1]: This divides the result from step 2 by the result from step 3. This fraction represents the portion of the principal you pay off each month, including interest.

- P [ i(1 + i)^n ] / [ (1 + i)^n – 1]: Finally, multiply the principal loan amount (P) by the result from step 4. This gives you your monthly payment (M).

Using a spreadsheet program like Excel or Google Sheets makes this calculation easy. They have built-in functions like PMT (Payment) that automatically calculate the monthly payment based on the principal, interest rate, and loan term.

Real-World Use: Troubleshooting & Negotiation

Understanding the formula is powerful in real-world scenarios:

- Verifying Loan Accuracy: Input the values from your loan agreement into the formula or a PMT function in a spreadsheet. If the calculated monthly payment doesn't match what the lender quoted, investigate further. There might be hidden fees or errors in the loan agreement.

- Evaluating Different Loan Options: Calculate the monthly payment and total interest paid for different APRs and loan terms. This helps you determine which option best fits your budget and long-term financial goals.

- Negotiating Loan Terms: Knowledge is power. When armed with the ability to calculate payments and understand the impact of different parameters, you can negotiate more effectively with lenders. Ask about lowering the APR, increasing the down payment, or shortening the loan term to save money on interest.

- Refinancing Analysis: Determine if refinancing your car loan is beneficial. Calculate the potential savings by comparing the current monthly payment and total interest paid with those of a new loan with a lower APR or shorter term.

Basic Troubleshooting: What if the numbers don't match?

If your calculated payment doesn't match the lender's quote, here's what to check:

- Hidden Fees: Are there any hidden fees rolled into the loan? Ask for a detailed breakdown of all fees.

- Incorrect APR: Double-check the APR used in your calculation against the APR stated in the loan agreement.

- Incorrect Principal: Ensure the principal loan amount accurately reflects the car price minus any down payment, trade-in value, or rebates.

- Rounding Errors: Minor discrepancies might arise due to rounding. However, significant differences warrant further investigation.

Safety: Beware of Loan Sharks

While calculating your monthly payment seems straightforward, some lenders may use predatory practices. Be cautious of loans with excessively high APRs, hidden fees, or unclear terms. Always read the fine print carefully and seek advice from a financial advisor if needed. Loan agreements are legally binding documents; don't sign anything you don't fully understand.

High APRs are especially dangerous. Even seemingly small increases in APR can significantly impact the total interest paid over the loan term. Always shop around and compare loan offers from multiple lenders before making a decision.

Final Thoughts

Understanding how your monthly car payment is calculated empowers you to make informed financial decisions. By mastering the formula and knowing the key components, you can verify loan accuracy, evaluate different options, negotiate effectively, and avoid potential pitfalls. This knowledge is as valuable as any tool in your garage when it comes to maintaining your financial health.

We have a detailed spreadsheet template that can help you calculate your monthly payments and compare different loan scenarios. This template includes the formula and allows you to input different variables to see how they affect your payment. If you'd like to download it, [provide download link or instructions here].