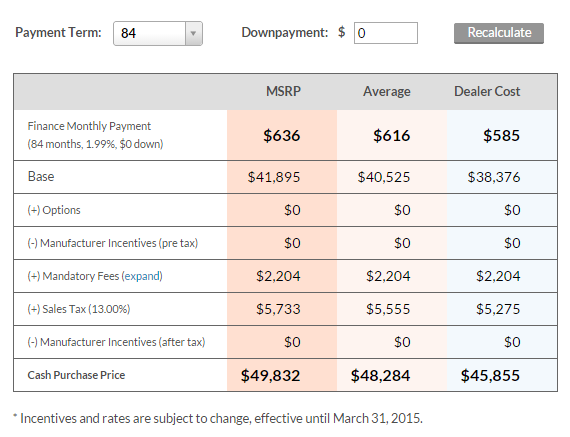

How To Determine Your Car Payment

Alright, let's talk about something just as important as horsepower and torque – your car payment. Knowing how it's calculated is crucial, whether you're planning a new purchase, refinancing, or just want a better handle on your finances. Understanding the mechanics behind your auto loan empowers you to negotiate effectively, avoid getting ripped off, and make informed decisions about your vehicle.

Purpose – Deciphering the Financial Engine

Thinking of this breakdown like a wiring diagram for your bank account, understanding your car payment isn’t just about knowing the monthly number. It’s about knowing where that number comes from. This knowledge is essential for:

- Negotiating Better Loan Terms: Armed with the knowledge of how interest rates and loan durations affect your payment, you can negotiate more effectively with lenders.

- Refinancing Strategically: Understanding your loan terms allows you to identify opportunities for refinancing to lower your interest rate or monthly payment.

- Budgeting Accurately: A clear understanding of your car payment allows for accurate budgeting and financial planning.

- Avoiding Scams and Predatory Lending: Knowledge of how loan terms work helps you identify and avoid potentially predatory lending practices.

- Making Informed Purchase Decisions: By understanding the impact of different vehicle prices, down payments, and loan terms, you can make informed purchase decisions that fit your budget.

Key Specs and Main Parts of Your Auto Loan

Let's break down the core components that determine your car payment:

- Principal (P): This is the initial amount of money you borrow to purchase the car. It's essentially the price of the car minus your down payment and any trade-in value.

- Annual Interest Rate (R): The percentage charged by the lender for borrowing the money. This is expressed as an annual rate, but we'll need to convert it for monthly calculations. A lower interest rate translates to a lower monthly payment and less overall interest paid.

- Loan Term (N): The length of time you have to repay the loan, typically expressed in months (e.g., 36 months, 60 months, 72 months). A longer loan term means lower monthly payments, but you'll pay more interest over the life of the loan.

- Monthly Interest Rate (r): The annual interest rate (R) divided by 12 (the number of months in a year). This is the rate used to calculate the interest portion of your monthly payment. r = R / 12

- Number of Payments (n): The total number of payments you'll make over the life of the loan. This is simply the loan term (N) in months. n = N

- Monthly Payment (M): The fixed amount you pay each month to the lender. This is the result of our calculations and the figure you're most concerned with.

The Formula - Auto Loan Payment Calculation

The standard formula for calculating your monthly car payment (M) is as follows:

M = P [ r(1 + r)^n ] / [ (1 + r)^n – 1]

Where:

- M = Monthly Payment

- P = Principal Loan Amount

- r = Monthly Interest Rate (Annual Interest Rate / 12)

- n = Number of Months in Loan Term

Let's break this formula down further:

* r(1 + r)^n: This part calculates the monthly interest rate multiplied by (1 + monthly interest rate) raised to the power of the number of payments. * (1 + r)^n – 1: This calculates (1 + monthly interest rate) raised to the power of the number of payments, then subtracts 1. * P [ r(1 + r)^n ] / [ (1 + r)^n – 1]: Finally, we multiply the principal loan amount by the result of the first calculation and divide it by the result of the second calculation. This gives us the monthly payment amount.How It Works: An Example

Let's say you borrow $25,000 (P) at an annual interest rate of 6% (R) for a loan term of 60 months (N).

1. Calculate the monthly interest rate (r): r = 6% / 12 = 0.06 / 12 = 0.005 2. Apply the formula: M = 25000 [ 0.005(1 + 0.005)^60 ] / [ (1 + 0.005)^60 – 1] M = 25000 [ 0.005(1.005)^60 ] / [ (1.005)^60 – 1] M = 25000 [ 0.005(1.34885) ] / [ 1.34885 – 1] M = 25000 [ 0.006744 ] / [ 0.34885 ] M = 25000 [ 0.019332 ] M = 483.32Therefore, your monthly payment would be approximately $483.32.

Real-World Use: Troubleshooting Your Loan

Here are a few scenarios where understanding your car payment calculation can be helpful:

- Payment Seems Too High: If your monthly payment seems significantly higher than you expected, double-check the interest rate, loan term, and any fees included in the loan. Use the formula above to calculate the expected payment based on the agreed-upon terms.

- Refinancing Opportunities: Keep an eye on interest rates. If rates drop significantly, consider refinancing your loan to a lower rate. This can save you a considerable amount of money over the life of the loan. Use an online refinance calculator to estimate the potential savings.

- Early Payoff: If you have extra cash, consider making additional principal payments to pay off your loan faster. This reduces the amount of interest you pay overall. Be sure to check if your loan has any prepayment penalties.

- Negotiating with the Dealer: Before finalizing a car purchase, negotiate the price of the car and the interest rate separately. Don't just focus on the monthly payment. A lower monthly payment achieved through a longer loan term can cost you more in the long run.

Safety: Avoiding Financial Hazards

The most significant risk is taking on a loan you can't afford. Before committing to a car loan, carefully assess your budget and ensure you can comfortably make the monthly payments. Don't get caught up in the excitement of buying a new car and overextend yourself financially. Be wary of loans with very long terms or high interest rates, as they can lead to financial hardship. Understand the terms and conditions of your loan, including any fees or penalties. Consider consulting a financial advisor if you have any concerns about your ability to repay the loan.

Moreover, be cautious of add-ons or extras that the dealer may try to include in the loan (like extended warranties or gap insurance). While some might be valuable, ensure you truly need them and that they're offered at a fair price. Don't let them inflate your principal unnecessarily.

Download Your Car Payment Breakdown Diagram

We’ve put together a detailed breakdown of the car payment calculation, including a handy spreadsheet you can use to experiment with different scenarios. It’s got the formula built in, so you can easily plug in your numbers and see how changes to the principal, interest rate, or loan term will impact your monthly payment.