How To Figure Out A Lease Payment

Leasing a vehicle can be a smart alternative to buying, especially if you like driving a new car every few years and aren't too concerned with building equity. However, deciphering the lease agreement and understanding how the payment is calculated can feel like navigating a complex engine diagram. This article aims to demystify the process, empowering you to understand the factors that influence your monthly lease payment and negotiate confidently.

Purpose: Why Understanding Lease Payment Calculation Matters

Just like understanding the internals of your car helps you diagnose problems and perform maintenance, understanding how your lease payment is calculated provides significant benefits. Here's why it's important:

- Negotiation Power: Knowing the underlying numbers gives you leverage to negotiate a better deal. You can identify areas where the dealer might be inflating figures and challenge them.

- Avoiding Hidden Costs: Leases can be filled with fine print. Understanding the calculations helps you identify and avoid unexpected fees or charges.

- Comparing Offers: When comparing lease offers from different dealerships, knowing the factors that influence the payment allows you to make an apples-to-apples comparison.

- Informed Decision Making: Leasing isn't for everyone. By understanding the financial implications, you can determine if it's the right choice for your budget and needs.

Key Specs and Main Parts of a Lease Payment Calculation

The lease payment is built upon several key components, acting as parameters. Think of these as the engine specs in your car. Change any of these, and it affects the overall performance (your monthly payment).

- MSRP (Manufacturer's Suggested Retail Price): The sticker price of the vehicle. This is the starting point for negotiations.

- Capitalized Cost (Cap Cost): This is the agreed-upon price of the vehicle for the lease. It's similar to the purchase price in a traditional car loan. It’s the negotiated sale price. You want to negotiate this down.

- Residual Value: The estimated value of the vehicle at the end of the lease term. This is determined by the leasing company (lessor) and is a key factor in calculating your payment. Higher residual values result in lower monthly payments. It's expressed as a percentage of the MSRP.

- Money Factor: This is the leasing company's interest rate, expressed as a decimal. To find the equivalent Annual Percentage Rate (APR), multiply the money factor by 2400. For example, a money factor of 0.00125 is equivalent to an APR of 3% (0.00125 * 2400 = 3).

- Lease Term: The length of the lease, typically expressed in months (e.g., 24, 36, or 48 months).

- Mileage Allowance: The number of miles you're allowed to drive during the lease term. Exceeding this allowance results in per-mile charges.

- Capitalized Cost Reduction (Cap Cost Reduction): This includes any down payment, trade-in equity, or rebates applied to reduce the capitalized cost. Think of this as putting money down on the car.

- Acquisition Fee: A fee charged by the leasing company to cover the costs of initiating the lease.

- Disposition Fee: A fee charged at the end of the lease term to cover the costs of processing the vehicle. This is often negotiable.

- Sales Tax: This varies depending on your location and is typically calculated on the monthly payment.

Symbols and Formula: Mapping the Lease Calculation

We can represent the lease calculation with a formula, similar to an engine diagram. It might look intimidating at first, but breaking it down makes it manageable:

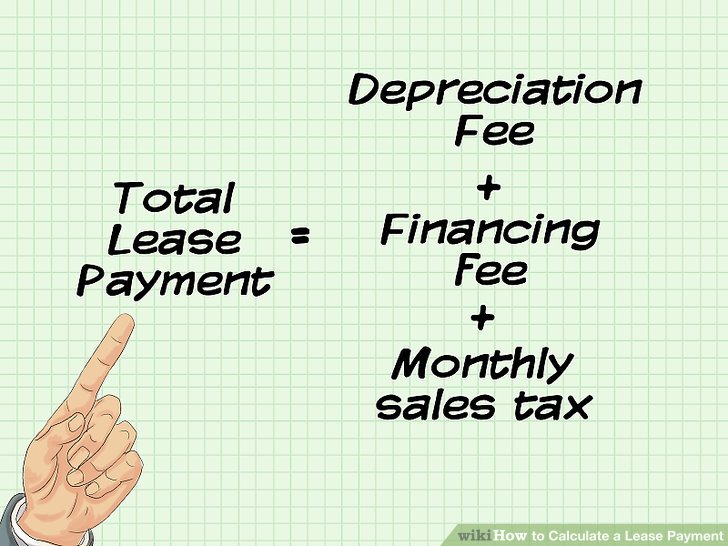

Monthly Lease Payment = Depreciation Fee + Finance Fee + Sales Tax

Let's dissect each component:

- Depreciation Fee = (Capitalized Cost - Residual Value) / Lease Term

- Finance Fee = (Capitalized Cost + Residual Value) * Money Factor

Interpreting the Symbols:

- + (Plus): Represents addition. These numbers contribute to the overall lease payment.

- - (Minus): Represents subtraction. Cap Cost Reduction lowers the capitalized cost, therefore lowering the payment.

- / (Division): Represents division. The Depreciation Fee divides the difference between the Cap Cost and Residual Value by the Lease Term to determine the monthly depreciation.

- * (Multiplication): Represents multiplication. The Finance Fee multiplies the sum of the Cap Cost and Residual Value by the Money Factor to get the monthly interest charge.

How It Works: The Lease Payment Engine in Action

Let's walk through an example to illustrate how the lease payment is calculated. Imagine you're leasing a car with the following specifications:

- MSRP: $40,000

- Negotiated Cap Cost: $36,000

- Residual Value (60% of MSRP): $24,000

- Money Factor: 0.00150 (equivalent to 3.6% APR)

- Lease Term: 36 months

- Capitalized Cost Reduction: $2,000 (trade-in equity)

- Sales Tax: 6%

First, we adjust the Capitalized Cost for the Cap Cost Reduction:

Adjusted Cap Cost = $36,000 - $2,000 = $34,000

Now, we can calculate the Depreciation Fee:

Depreciation Fee = ($34,000 - $24,000) / 36 = $277.78

Next, we calculate the Finance Fee:

Finance Fee = ($34,000 + $24,000) * 0.00150 = $87.00

Now, we add the Depreciation Fee and Finance Fee to get the pre-tax monthly payment:

Pre-Tax Monthly Payment = $277.78 + $87.00 = $364.78

Finally, we add sales tax:

Sales Tax = $364.78 * 0.06 = $21.89

Total Monthly Lease Payment = $364.78 + $21.89 = $386.67

Real-World Use: Troubleshooting and Negotiation Tips

Understanding the calculations allows you to troubleshoot potential issues and negotiate effectively:

- High Monthly Payment: If your monthly payment seems too high, scrutinize the money factor, capitalized cost, and residual value. A higher money factor or capitalized cost directly increases your payment. A lower residual value also increases it. Negotiate a lower sales price to reduce the capitalized cost.

- Low Residual Value: A low residual value means you're paying for more of the vehicle's depreciation. Research the expected residual values for the car you're leasing through resources like Edmunds or Kelley Blue Book. If the dealer's residual value is significantly lower, challenge it.

- Inflated Money Factor: The money factor is essentially the interest rate. Negotiate this down as much as possible. Know the average money factors for similar leases to have a benchmark.

- Unnecessary Add-ons: Dealers often try to add unnecessary options or packages to increase the capitalized cost. Decline these unless you genuinely need them.

- End of Lease: Plan ahead for the end of the lease. Are you responsible for excessive wear and tear? What is the disposition fee? Can you purchase the vehicle at the residual value? Knowing these factors ahead of time prevents surprises.

Safety: Risky Components and Hidden Fees

Just like certain engine components require extra caution, some aspects of a lease agreement can be risky if overlooked:

- Mileage Penalties: Exceeding your mileage allowance can result in substantial per-mile charges. Carefully estimate your annual mileage needs and choose a lease with an appropriate allowance.

- Excessive Wear and Tear: Leases typically have strict standards for acceptable wear and tear. Dents, scratches, and worn tires can result in costly repair charges at the end of the lease. Protect the vehicle and address any minor damage promptly.

- Early Termination Fees: Terminating a lease early can be extremely expensive. You'll likely be responsible for paying the remaining lease payments plus a penalty. Consider the long-term commitment before signing the agreement.

- Hidden Fees: Be wary of hidden fees such as documentation fees or vehicle preparation charges. Ask for a complete breakdown of all fees and negotiate to eliminate or reduce any unnecessary charges.

Leasing a car can seem daunting, but understanding the underlying calculations empowers you to make informed decisions and negotiate confidently. By understanding the role of each parameter and keeping an eye out for red flags, you can secure a lease that aligns with your needs and budget.

Remember, this is a simplified explanation. Always read the lease agreement carefully and consult with a financial advisor if you have any questions or concerns.

We have a more detailed version of this article and a downloadable PDF version of the formula. Contact us to get this valuable tool!