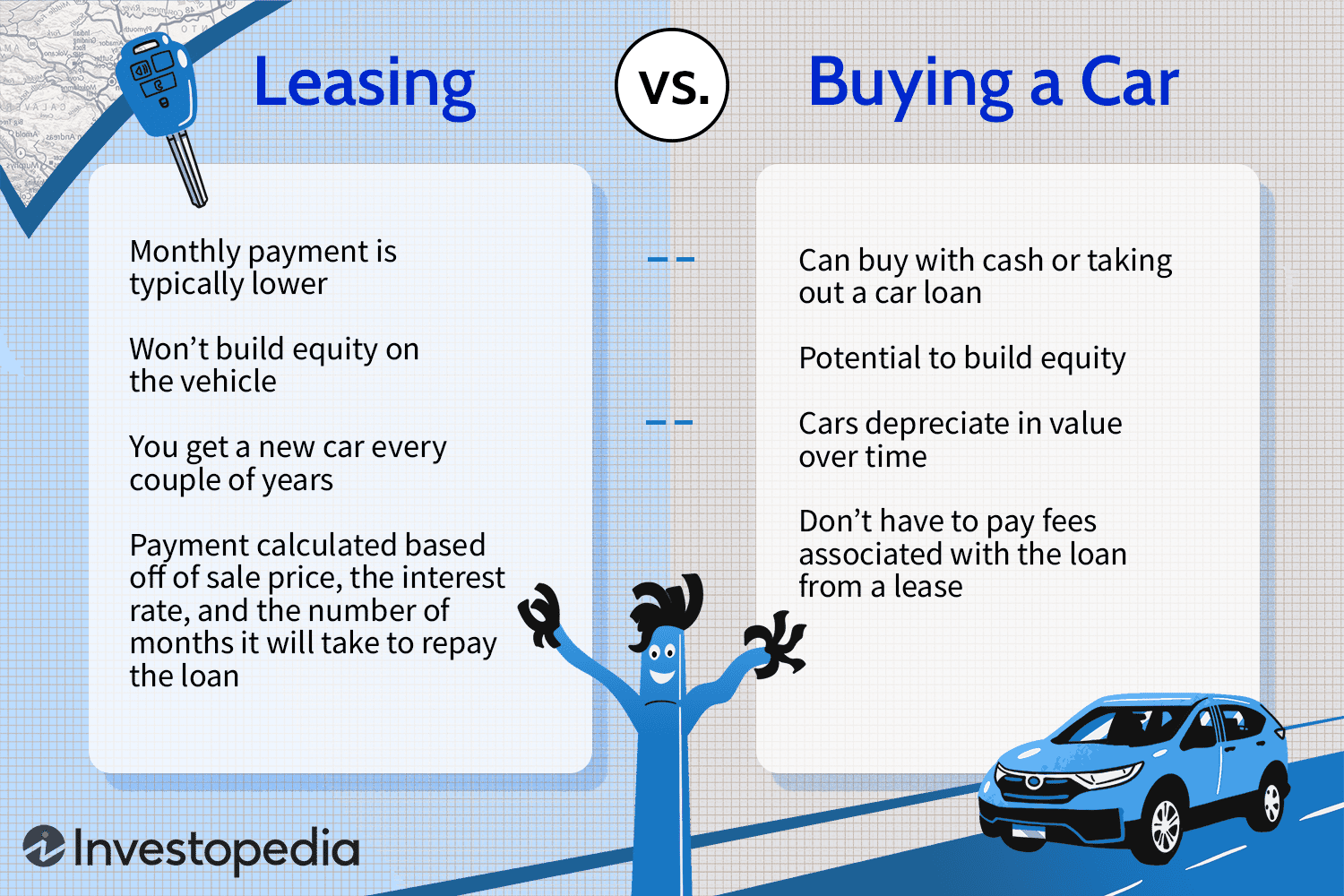

How To Qualify For A Car Lease

So, you're thinking about leasing a car? Excellent choice. It's a great way to drive a new vehicle without the long-term commitment of ownership. But just like diagnosing a tricky engine problem, understanding what it takes to qualify for a car lease is crucial. This isn't about just walking into a dealership and hoping for the best. It's about understanding the underlying mechanics of the leasing process, so you can be prepared and get the best possible deal. We're going to break down the essential factors, from credit scores to debt-to-income ratios, so you can approach the dealership with confidence.

Key Specs and Main Parts of Lease Qualification

Think of lease qualification as a complex equation with several key variables. These "variables" are the main factors lenders consider when deciding whether to approve your lease application. Let's look at the most important ones:

Credit Score: The Foundation

Your credit score is arguably the single most important factor. It's a numerical representation of your creditworthiness, based on your past borrowing and repayment history. Think of it as the engine block of the leasing process – if it's cracked, the whole thing falls apart. Lenders use credit scores to assess the risk of lending money to you. Generally, a higher credit score translates to lower interest rates (or in this case, a better money factor, which we'll discuss shortly) and a higher likelihood of approval. A good to excellent credit score, typically above 700, is generally required for the best lease deals. Scores in the mid-600s might still get you approved, but the terms won't be nearly as favorable. Scores below 600 will likely result in denial.

Debt-to-Income (DTI) Ratio: Your Financial Breathing Room

The Debt-to-Income (DTI) ratio is the percentage of your gross monthly income that goes towards paying debts, including credit card bills, student loans, mortgages, and any other recurring obligations. A lower DTI indicates that you have more disposable income and are less likely to default on your lease payments. Lenders typically prefer a DTI of 43% or lower, but some may go higher depending on other factors like your credit score and down payment. Calculate your DTI by dividing your total monthly debt payments by your gross monthly income.

Down Payment: Not Always Required, But Often Helpful

Unlike buying a car, a significant down payment isn't always required for a lease. However, putting money down can lower your monthly payments and potentially improve your chances of approval, especially if your credit score isn't perfect. Think of it as giving the lender a bit of reassurance – you're showing them you have "skin in the game." Keep in mind, though, that down payments on leases are generally non-refundable, so weigh the pros and cons carefully.

Lease Term: The Length of the Agreement

The lease term is the length of the lease agreement, typically expressed in months (e.g., 24 months, 36 months, or 48 months). Shorter lease terms usually result in higher monthly payments, while longer terms typically have lower payments. The ideal term depends on your individual circumstances and how long you want to be committed to the vehicle. It's like choosing the right gear ratio – you need to find the balance that works best for your driving style and needs.

Money Factor: The "Interest Rate" of a Lease

The money factor is the equivalent of an interest rate in a lease agreement, although it's expressed as a small decimal. It represents the cost of borrowing the car for the duration of the lease. To calculate the approximate annual interest rate, multiply the money factor by 2400. A lower money factor means you'll pay less interest over the lease term. Negotiating a lower money factor is crucial to getting a good lease deal. This is akin to adjusting the fuel-air mixture - get it right, and you get optimal performance (i.e., a lower payment).

Residual Value: What the Car Is Worth at the End of the Lease

The residual value is the estimated value of the car at the end of the lease term, expressed as a percentage of the car's original MSRP (Manufacturer's Suggested Retail Price). A higher residual value means you'll pay less in depreciation over the lease term, resulting in lower monthly payments. The lender sets the residual value based on factors like the make, model, and projected depreciation rate of the vehicle. This is like estimating the resale value of a modified car – factors like popularity and condition play a big role.

How It Works: The Leasing Process

Qualifying for a car lease involves several steps, similar to diagnosing a complex automotive issue:

- Credit Check: The lender will run a credit check to assess your creditworthiness. This is like hooking up a diagnostic scanner to read the error codes.

- Income Verification: The lender will ask for proof of income, such as pay stubs or tax returns, to verify your ability to make the lease payments. This is like verifying the voltage output of the alternator.

- Debt Assessment: The lender will assess your existing debts to calculate your DTI ratio. This is like checking for vacuum leaks – you want to make sure everything is running efficiently.

- Approval and Terms: If you're approved, the lender will provide you with the lease terms, including the monthly payment, lease term, money factor, and residual value. This is like receiving the final repair estimate.

- Negotiation: You can negotiate the lease terms, such as the money factor, down payment, and any add-on fees. This is like haggling with the parts store for the best price.

- Contract Signing: Once you're satisfied with the terms, you'll sign the lease agreement. This is like finalizing the repair order.

Real-World Use: Basic Troubleshooting Tips

Let's say you're denied for a lease. What can you do? Here's some basic troubleshooting:

- Check Your Credit Report: Obtain a copy of your credit report from all three major credit bureaus (Equifax, Experian, and TransUnion) and check for any errors or inaccuracies. Dispute any errors you find.

- Improve Your Credit Score: Pay down your existing debts, make all your payments on time, and avoid opening new credit accounts.

- Lower Your DTI: Pay off some of your existing debts or increase your income.

- Increase Your Down Payment: A larger down payment can offset a lower credit score or higher DTI.

- Consider a Co-Signer: If you have a friend or family member with good credit, they may be willing to co-sign your lease.

- Shop Around: Different lenders have different requirements, so shop around for the best possible deal. Don't settle for the first offer you receive.

If you have a lower credit score, focusing on improving it is like rebuilding an engine – it takes time and effort, but the results are worth it. Be patient and persistent, and you'll eventually qualify for the lease you want.

Safety: Highlighting Risky Components

One of the biggest "risks" in leasing is not fully understanding the terms of the agreement. Be especially cautious about the following:

- Excess Mileage Charges: Leases typically come with a mileage limit. Exceeding this limit can result in hefty charges per mile.

- Excess Wear and Tear Charges: You're responsible for maintaining the vehicle in good condition. Excessive wear and tear, such as dents, scratches, or interior damage, can result in charges at the end of the lease.

- Early Termination Fees: Terminating a lease early can be very expensive. Be sure you're committed to the full lease term before signing the agreement.

- Hidden Fees: Watch out for hidden fees, such as acquisition fees, disposition fees, and documentation fees. Ask for a complete breakdown of all costs before signing the agreement.

Ignoring these "risks" is like neglecting to torque your lug nuts – it can lead to serious problems down the road. Read the lease agreement carefully and ask questions about anything you don't understand.

By understanding the key factors involved in lease qualification and taking proactive steps to improve your creditworthiness, you can increase your chances of getting approved for the lease you want and driving away in your dream car. Think of it as tuning your financial engine for optimal performance on the leasing track.

We have a detailed qualification diagram available for download. This diagram visually represents all the factors discussed above and provides a handy reference guide for navigating the leasing process.