Whats A Good Monthly Car Payment

Let's talk about a topic that can be more complex than diagnosing a misfire: determining what constitutes a good monthly car payment. Unlike engine diagnostics, which involves tangible parts and testable parameters, car payments involve personal finance, credit scores, and a dash of economic forecasting. This isn't a simple torque spec – it's a balancing act between affordability and your automotive aspirations.

Purpose: Why Understanding Car Payments Matters

Understanding the anatomy of a car payment goes beyond simply knowing the monthly amount. It's about financial literacy. Ignoring this aspect can lead to financial strain, negative equity (being "upside down" on your loan), and even repossession. Just as you wouldn't haphazardly modify your engine without understanding its components, you shouldn't commit to a car loan without understanding the factors at play.

A well-informed approach allows you to:

- Negotiate effectively: Armed with knowledge, you can haggle on the vehicle price, interest rate (APR), and other fees.

- Avoid overspending: Understand what you can realistically afford, preventing future financial hardship.

- Plan for the future: Factor in the long-term costs of car ownership (insurance, maintenance, fuel) and plan accordingly.

- Build credit: Responsible car loan management can positively impact your credit score.

Key Specs and Main Parts of a Car Payment Calculation

Let’s break down the key elements that contribute to your monthly payment, similar to how you would identify the critical components of an engine before a rebuild:

1. Principal (Loan Amount):

This is the amount of money you borrow to purchase the vehicle. It’s the net price of the car after any down payment or trade-in credit. The lower the principal, the lower the monthly payment, all other factors being equal.

2. Interest Rate (APR - Annual Percentage Rate):

The interest rate is the cost of borrowing the money, expressed as a percentage. This is arguably the most important factor. A seemingly small difference in APR can translate to thousands of dollars over the life of the loan. Your credit score heavily influences the APR you'll receive.

3. Loan Term (Duration):

This is the length of time you have to repay the loan, usually expressed in months (e.g., 36 months, 60 months, 72 months). Longer terms result in lower monthly payments but higher total interest paid. Shorter terms mean higher monthly payments but lower overall interest. Consider it like gear ratios; longer terms provide "lower gearing" for affordability, but shorter terms provide "higher gearing" for quicker payoff.

4. Down Payment:

The initial amount you pay upfront. A larger down payment reduces the loan amount and can potentially lower your interest rate.

5. Taxes and Fees:

These can include sales tax, registration fees, documentation fees, and other charges levied by the dealer and government. Always factor these into your total cost calculation. They’re akin to the “hidden costs” of a project – always plan for them!

6. Trade-In Value (If Applicable):

The agreed-upon value of your existing vehicle, which reduces the principal of your new loan. Be realistic about your trade-in's condition; dealers will thoroughly inspect it.

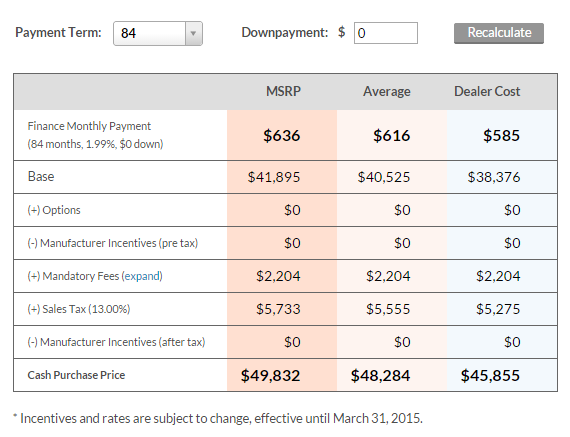

How It Works: The Math Behind the Payment

The monthly car payment is calculated using a standard amortization formula. Don't panic – you don't need to memorize it! There are plenty of online car loan calculators that will do the math for you. However, understanding the formula provides valuable insight.

The formula is as follows:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Monthly Payment

- P = Principal Loan Amount

- i = Monthly Interest Rate (Annual Interest Rate / 12)

- n = Number of Months (Loan Term)

While the formula looks intimidating, it's essential to understand that the calculator performs this automatically. The key is to input accurate values for P, i, and n to get a realistic estimate of your monthly payment. Manipulate these values to see how they impact the outcome. For example, try increasing your down payment and observe the effect on your monthly payment and total interest paid. It's like adjusting the air/fuel ratio on your carb – small tweaks can have significant results.

Real-World Use: Troubleshooting Car Payment Calculations

Let's address some common scenarios:

- "I'm getting different payment amounts from different calculators!": This is common. Ensure you're using the same values for principal, APR, and loan term. Also, some calculators might include taxes and fees, while others don't. Clarify what each calculator includes.

- "The dealer's payment is much higher than my estimate!": This could be due to several factors: the dealer might be marking up the interest rate, adding on hidden fees, or inflating the price of add-ons. Scrutinize the loan paperwork carefully.

- "I can't afford the payment I calculated!": Reassess your budget. Consider a less expensive car, increasing your down payment, or shopping around for a lower interest rate. Don't stretch yourself too thin.

A general rule of thumb is the 20/4/10 rule: 20% down payment, loan term of 4 years or less, and no more than 10% of your gross monthly income spent on transportation costs (including car payment, insurance, and fuel). While not a strict guideline, it's a good starting point.

Safety: Risky Components to Watch Out For

Just like certain engine components can be dangerous if mishandled (e.g., airbags), certain aspects of car loans can be financially risky:

- High APR: This significantly increases the total cost of the loan. Shop around for the best rates.

- Long Loan Term: While it lowers the monthly payment, you'll pay far more interest over the life of the loan and increase the risk of being upside down.

- Negative Equity: If you trade in a car with negative equity, that amount gets rolled into your new loan, increasing your debt.

- Add-ons: Extended warranties, paint protection, and other add-ons can inflate the price of the car and often have low value.

- Balloon Payments: Be wary of loans with large balloon payments at the end of the term. If you can't afford the balloon payment, you'll need to refinance.

Always read the fine print and understand all the terms and conditions of the loan before signing anything. Don't be pressured into making a decision you're not comfortable with. Treat it like inspecting a used engine – look for red flags and don’t be afraid to walk away if something doesn't feel right.

Ultimately, a "good" monthly car payment is one that fits comfortably within your budget and allows you to meet your other financial obligations without undue stress. It requires careful planning, research, and a realistic assessment of your financial situation. Don’t hesitate to consult with a financial advisor for personalized guidance. Just like tuning your car, financial planning requires expertise and attention to detail.